Buy Low and Sell High. Really!

Gregory V. Milano | June 10, 2009

“What’s that? Then sell! Oh, they’re selling? Then buy!” Sound like Warren Buffett, Peter Lynch or George Soros? No, these shrewd investment remarks bellowed from Rodney Dangerfield in the 1980 comedy, Caddyshack. Audiences laughed because it was absurdly obvious. If everyone is buying, then sell, and if everyone is selling, then buy.

Tell that to corporate America! In one of the greatest economic mysteries of our time, most acquisitions happen when prices are high and the checkbooks close when prices decline. Shareholders are and should be outraged.

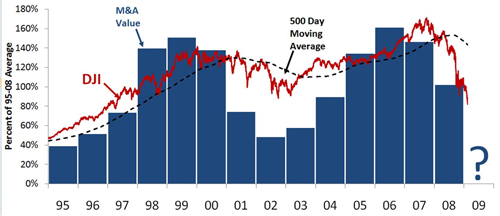

The above chart shows that during the six peak M&A years (1998-2000 and 2005-2007), dollar volumes were nearly 220% of the surrounding years. This enormous transaction volume transpired despite the Dow Industrials Index averaging 28% higher in these years. Seems more like “Buy High” than “Buy Low”!

In the first quarter of 2009, the Dow hovered at such low levels that the 2007 peak represented 60-120% upside and yet M&A had nearly ground to a halt. How many CEOs will look back in a few years, as they did during the last peak, and wish they had bought low while they had the chance? In fact, now may be the opportunity of a lifetime for making low priced strategic acquisitions.

While most corporate leaders agree in principle that now is a good time to buy, and a few are beginning to act on this intuition, most continue to play the “wait and see” game on the economic recovery. Those that wait will miss the opportunity. We don’t know when it will come, but the market will likely rise substantially before we are sure the economy is picking up.

Ignore these comments if you are a trader. Neither I nor anyone can assure you we have seen the bottom. Indeed many thought we were there when the Dow Jones Industrial Index broke through 9000, 8000, and 7000. Who knows? The current market has generated numerous investment ideas that may or may not be attractive short term stock picks, but are surely good investments for those that buy and hold. M&A is the ultimate buy and hold strategy.

So what are the potential reasons for a noticeable decline in acquisition investing during periods of depressed valuations? Is it a shortage of capital? According to Capital IQ, global public non-financial companies held over $2.3 trillion in cash and short term investments at the end of the last fiscal year. Over $650 billion of that was held by US companies.

Beyond cash on the balance sheet, many have the capacity to access the capital markets as demonstrated by recent debt and equity offerings. There is also a treasure trove of private equity funding – by some estimates over $400 billion. Yet the M&A markets have been comatose. Rodney would have found this to be a wonderful time to buy!

So if it’s not a lack of capital, perhaps the problem is not buyers, but sellers who are unwilling to sell at low prices. That may have been true at the bottom, but as the market has risen companies have started issuing stock again, indicating they are less uncomfortable with their share price. Equity issuance by non-financials jumped almost three fold in May and June over the first four months of 2009. Perhaps sellers can be found after all.

So why is there so little M&A?

This dilemma is potentially the result of an over-reliance on efficient market theory. The efficient market beliefs held by many may be the problem! This revered theory relies on an assumption of rational behavior in humans. Yet psychological research shows that humans often extrapolate and overreact which feeds economic bubbles and troughs.

Does the notion of efficient markets imply the market is always right? In reality, although the efficient market testing holds up pretty well for individual stock picking, the overall market seems to overreact at both peaks and troughs and is all but efficient.

Professor Lo, Director of the MIT Laboratory for Financial Engineering, and other leading academic thinkers have introduced emotion and overreaction into their models of the market. They no longer assume market participants are calm, cool and calculating. And many of us applaud this trend.

Are market bubbles and troughs excessively influenced by the youth and inexperience of a few analysts and traders on Wall Street? How many of them were around on Black Monday in 1987? Not a high percentage, to be sure, but if trader naiveté were the problem, wouldn’t experienced corporate executives be making money hand over fist by buying when these inexperienced traders sell and vice versa?

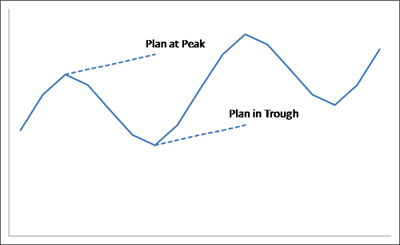

Indeed corporate planning can suffer the same irrationality. Over the last two decades I have seen hundreds of management plans that show steady growth regardless of the cycle, even in cyclical businesses.

Nobody seems to see the cycle at the time, but when we look back, the cycles always seem obvious. We all “knew” the market was overvalued in 1999. And when we look back in a few years, we will all “know” the market was undervalued in Q1 2009.

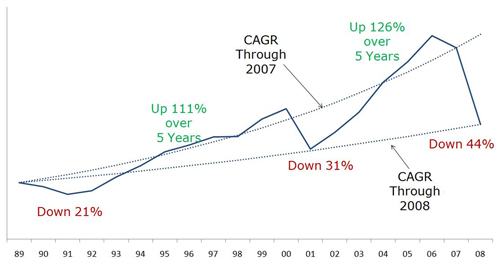

The S&P 500 high was just over 1565 on October 9, 2007, four months after the start of the credit crisis. The low (so far) was 677 on March 9, a decline of 57% off the peak. That’s quite a loss of value. The peak itself may have been excessively high, but most of the drop can be attributed to a loss of intrinsic value due to the economy and a downward overreaction.

The media is flooded with seers waxing eloquently about how the current economic crisis coupled with the financial market freeze will leave a deep prolonged corporate profit eroding recession in its wake. This may be but was a 57% loss of value justified?

To test the reasonableness of the market, we applied a simple valuation model to the current situation.

A straightforward Price/Earnings Growth (PEG) valuation model can be used to estimate what investors are expecting. And for sophisticated investors and corporations using thoughtful free cash flow valuation, even more insights become apparent.

In the PEG model, with earnings of $1.00 per share (EPS) that are expected to grow by 5% (g) per year over the long term and an overall expected return of 10% over time (Ke), the price valuation would be:

EPS $1.00

Price = ——— = ——— = $20

Ke - g 10%-5%

Under these conditions, the example company is expected to trade at a Price/Earnings Ratio of 20x. The share price of $20 is the present value of $1.00 growing at 5%, and a 10% return would be earned each year if everything rolls forward as expected.

Note that only 5% of the $20 share price can be explained by the current earnings and the balance is derived from the long term earnings outlook, on a present value basis. Small swings in that long forecast can cause sharp movements in share price.

To test the expected impact of a substantial economic crisis, assume earnings drop by 44% as has happened to the S&P 500 through 2008 (2009 estimates are up 13%). It is clear this erodes value. That is, if the share price stayed the same we would earn less than 10% so the share price must decline. How can we determine the size of the decline in price required to get us back to a 10% expected overall return?

The last two downturns were not as severe, but the earnings over the next five years grew a cumulative 118% on average. And the deeper downturn led to a stronger recovery, as cycles tend to do.

So how much should the market drop if earnings decline 44% and there is 118% earnings recovery over the ensuing five years? If we assume long term growth remains 5%, our model shows the share price dropping about 10% to $18.04. And if we assume only half the earnings growth over the next five years, the decline in our valuation is 32% to $13.59. This may be conservative as deeper declines tend to lead to stronger recoveries – the inverse of the higher you rise the farther you fall.

So, why the 57% decline? In a word, FEAR.

Investors fear the economy may never recover. We are in the midst of a crisis in both the real economy and in the financial markets. Many fear the deleveraging of financial markets will reduce demand and add considerable delays and uncertainties regarding “if and when” there will be a recovery.

What does this mean for those of us who believe the economy will get back on track eventually? Simply step up our 10% expected return to the level the market has priced in for risk. In fact, it is straightforward to solve for the required return that links our earnings outlook to the actual share price.

In our example we must step up our required return to 13-15% to explain the 57% decline. In other words, we expect a 3-5% premium return in today’s markets which would sound good to Rodney!

There are more sophisticated models for estimating market embedded required returns, but this simple model explains the market mechanism adequately to understand that for those who believe the economy will emerge eventually, the expected returns are the highest in many years.

Many investors are starting to see this logic and the fear is subsiding even though we still cannot see solid indicators of recovery. As of June 9, just three months after the bottom, the S&P index is up to 942, a 39% rise off the bottom of the trough. Said differently, the index has recouped 265 points, or 30 percent of the decline. So it’s not too late.

What does this mean for strategic corporate acquisitions and other investments? Good news on several fronts. Now is the time to consider buying because:

-

Prices in many industries are still very low by historical standards, even after adding a possibly large acquisition premium.

-

Prices have started rising so the psychology of selling too low has been softened and some deals can be struck.

-

Capital markets have begun opening up so even those without enough cash can play the game.

-

Many organic investments such as plant, equipment, research, training and the like are also attractive at this time as the same economic forces are at work in these markets, they are just less observable.

So how should executives proceed? Start by evaluating your strengths and ways you can create value by flexing your core competencies through small or large acquisitions and organic investments at very attractive prices. Management must evaluate where they have the ability to manage well and deliver returns above the cost of capital, and then look for growth options in those areas.

But what types of growth are likely to create value – both in terms of immediate share price impact and in realized operational value growth over time? The means of growing can be organic or acquisitive but it must show the promise of generating returns over the cost of capital over time.

Fortunately, the current difficult economic environment illuminates strong versus weak businesses.

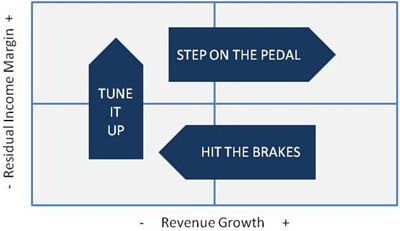

As a framework for strategic evaluation of financial performance, we have developed a simple two by two matrix. On the vertical axis we measure Residual Income Margin, or RIM. This is simply the cash flow a business generates less the cost of capital employed, shown as a percent of sales. On the horizontal axis we measure forward revenue growth.

A few simple insights come from this:

Hit the Brakes: For businesses unable to deliver sustained positive residual income, investments in growth must be stopped until the business earns the right to grow. One CEO told me his goal was to stop repeatedly approving 25% return projects in businesses that somehow keep delivering returns of only 6%. Spot on.

Tune it Up: Once growth investment is shut down, a negative RIM business must pursue cost and capital efficiencies to earn their right to grow. True, this article is about growth and here comes the efficiency plea but in businesses that cannot cover the cost of capital, we shouldn't plow in more capital. It’s tempting to use growth as a means of improving RIM by absorbing fixed costs, but this rarely works, otherwise large companies would have much lower G&A than smaller peers.

Step on the Pedal: Positive RIM companies need to grow to realize their true value creation potential. The higher the RIM, the more value is added by growth. For multi-business companies, this is where the core competencies are and investments should be targeted to these businesses in a big way. This can be in the form of acquisitions, capital expenditures, research, marketing, training and the like. All of these investments are at attractive prices in most industries now.

Many companies have figured out how to Hit the Brakes and Tune it Up but surprisingly, many are hesitant to Step on the Pedal and do not put enough resources behind growth in their strongest businesses. This is the most common strategic error I have witnessed over the last two decades. Invest to grow your profitable businesses!

Perhaps companies emphasize cost cutting more than growth because it’s easier to predict the outcome. Conjecture on future revenues from a growth plan can be challenging and fraught with second guessing. The short term nature of CEO tenures and real and perceived incentives further discourages entrepreneurism and growth investments when the payoff is over time. Rhe media and some Wall Street analysts might be to blame a bit too.

Another distraction from growing can be an obsession with percent rates of return, especially in high return businesses, due to fears of diluting returns. Investing at 25% when the underlying business earns 40% will add value.

To be successful, management must overcome these obstacles, decide where the value creation opportunities are, identify prospects and pursue strong growth investment strategies during this time of relatively low investment cost. Those that live by this paradigm will actually “Buy Low and Sell High”. Really!

Gregory V. Milano is Co-Founder and Chief Executive Officer of Fortuna Advisors LLC

gregory.milano@fortuna-advisors.com |